Have you ever wondered which you should look into first when considering home ownership: the actual property itself or the home loan? It’s easy to get carried away with the fun part of buying a property – looking at houses and imagining your future – but delaying the less compelling task of arranging finance will weaken your negotiating position on both the property and the loan.

Looking for a property to purchase is an exciting time. Choices regarding location, size, number of rooms and local amenities often see

house hunters carried away in the excitement of daydreams and anticipation. But, before you get too carried away, it’s important to check

off the essentials first. Although organising your finances may seem drab in comparison to perusing sales listings, gaining pre-approval

with a lender will give you confidence about how much you can afford to borrow.

First and foremost, you need to determine if you’re eligible to borrow money from a lender. Your ability to repay the loan will need to be

assessed – you don’t what to find out after you’ve made an offer that your credit history or deposit is not up to scratch.

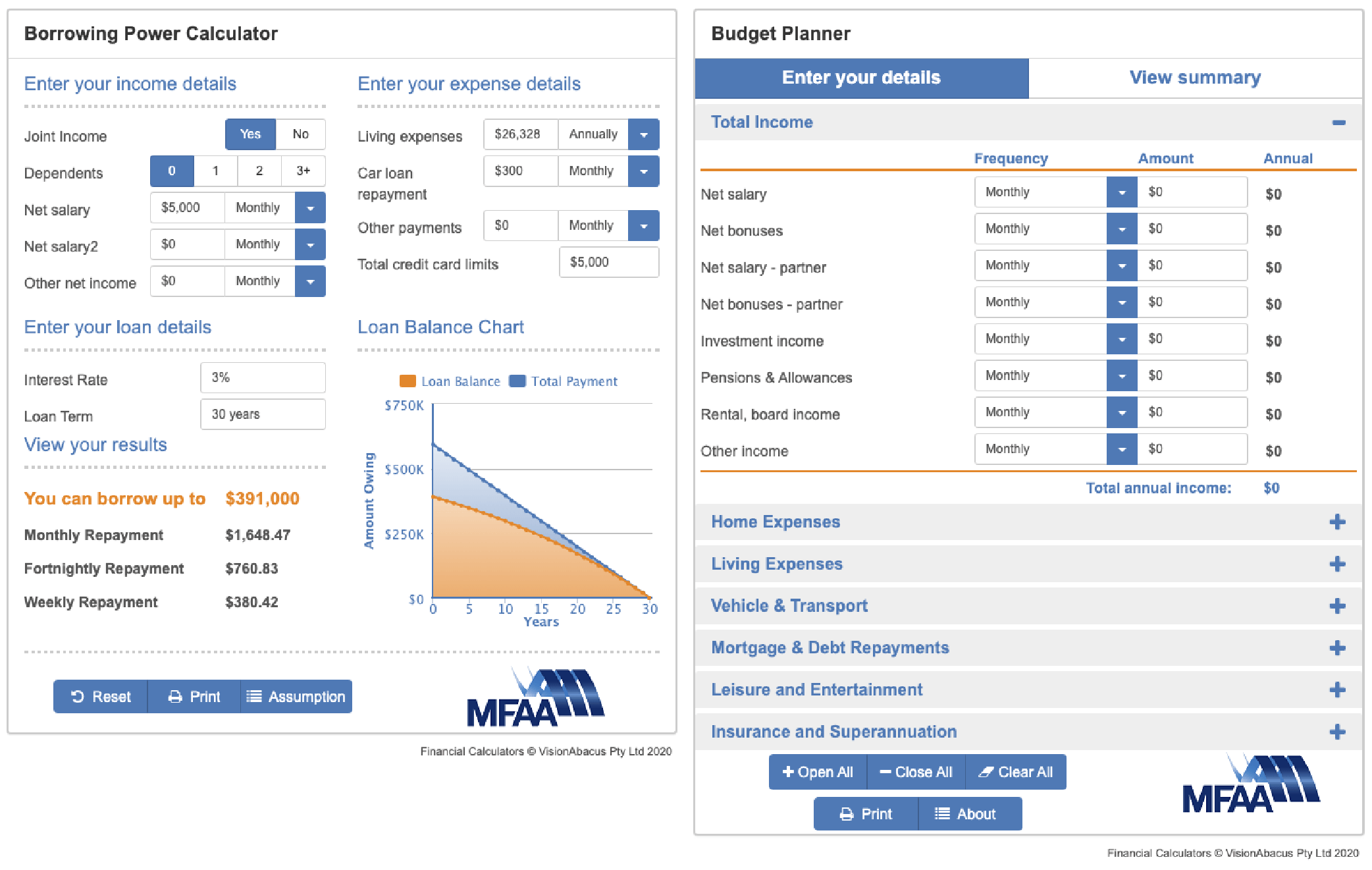

Our range of handy online calculators can help with that, allowing you to quickly provide a guide about your borrowing

power,

loan repayments, how

long to repay, home loan offset,

budget planning, and saving.

Arranging finance before finding the perfect property will put you in a good position when it comes time to make an offer. When you do find

the house you have always wanted, you can present to the seller and estate agent as a prepared applicant who is serious and reliable.

It shows you mean business, and gives them peace of mind that your financing will not fall through. Don’t be afraid to let the selling agent know you have conditional loan approval in place. If you're unsure of what type of loan to apply for or that you might be eligible for, speaking with a mortgage broker is one of the easiest steps to becoming more financially empowered and knowledgable.

Sellers are most interested in completing their sale fuss-free and with steadfast funding, and showing that you are capable of both will help put you at the top of a potentially competitive list of applicants. In the instance that you find and secure purchase of a home without having your loan pre-approved by a lender, there are a few pitfalls that you risk running into.

If you don’t have financing to pay for your property, you run the risk of forfeiting your initial 10% non-refundable deposit you need to put down to secure the property. While this fee may differ depending on what state you live in, but the point is that it always pays to be organised and have pre-approval in place. With this house deposit fee being one of the biggest lump sums many people transfer in their lives, this puts more pressure on being able to pay it and follow through with the deal, so you don't set yourself back financially.

Saving home loan applications to the last minute also leaves less time to find the most suitable loan and have it approved ahead of

settlement. Arranging financing as an afterthought also adds immense pressure to the process of shopping around for the right loan and

gathering the paperwork to prove you can service the loan. You don’t want to rush this process. Home ownership is a big step in life, that

requires careful time, planning, and strategy.

The first step towards finding your new home is speaking to a finance broker to sort out all the details, answer any questions you might have, and give you invaluable tips to make the process as smooth and simple as possible. Our accredited team at Acquired Home Loans are ready to help, with a wealth of experience, so feel free to contact us to discuss your situation so you can get back to the exciting anticipation of moving in to your home, rather than caught up on all the tricky finances.

First Home Buyer

10 Tips for Property Investors

Moving Checklist

"My brother and I purchased an investment property from Acquired after being recommended by a

friend. Their research, customer service and professionalism made the process simple and easy. We wouldn't hesitate buying through

them again."

Justin Furno

"Initially I was unsure of how to build a property investment portfolio, however Acquired

were helpful, approachable and listened to my concerns; explaining everything in simple terms."

Evon Kong

"Acquired made a great impression with their expertise and knowledge. Their

professionalism is just one of the reasons why I chose them to help expand, and look after my property portfolio."

Paola Astudillo

"Acquired made a great impression with their expertise and knowledge of property

investment. Their professionalism is just one of the reasons why I chose them to help expand, and look after my property

portfolio."

Paola Astudillo

"I highly recommend Acquired for all your investment needs. They are true professionals with

outstanding business acumen and integrity."

Richard Narria

"My brother and I purchased an investment property from Acquired after being recommended

by a friend. Their research, customer service and professionalism made the process simple and easy. We wouldn't hesitate

buying through them again."

Justin Furno